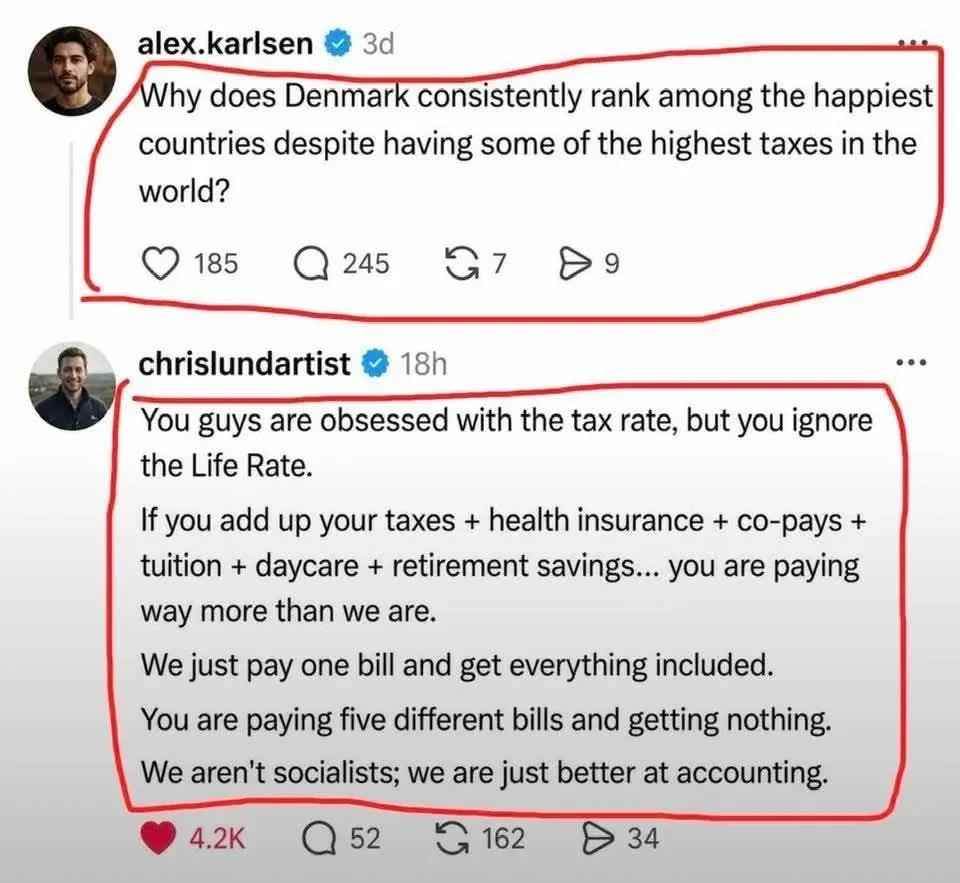

I did the math in the USA. When I was married with kids my effective rate for a the highest year was 52%. My last year as a single male and all kids over 26, it was 46%. Effective, not marginal, because that matters in the USA as we don’t track those “other salary deductions” for taxes. Effective for those ready to argue include stupid shit like deductibles, copays, uncovered care, out of network care (that happens more than you think with kids). one year we spent 40k (max. In network deductible) because one of my kids had a spiral fracture of his leg on a growth section that had he not endured 3 (THREE) surgeries, he would be left side shorter. That was 190k for all surgeries and 40k out of pocket. Dental, HSA, FSA, Vision, Medical… People need to realize that even though its pre tax, you’re still paying for it and that needs to be considered for effective rate.

I was offered a job in Denmark, so I know this for fact: Denmark was a near match at marginal rate to USA effective rate assuming I never needed critical care in the USA (i would be in debt). BUT, Denmark has effective tax rates in the 40% for those making less than 85k (USD). I think there’s a rich person tax above that at 49%, but I never accepted the job because my Ex wife was a shithead so I didn’t find out.

I’m now in spain paying around 47% effective, but get Beckhams law will make that be 24% at tax time for the next 10 years. After that I need to pay like everyone else and at 10 years I get a pension (small one) for spain.

190k is a very large amount, I’m not sure if by 40k out of pocket you mean the insurance covered the rest.

Still, 40k is a lot of money and 190k is pretty much my salary for the next 10 years. I’m sure jobs are a bit better paid in the US; but I’m also quite convinced it is not that common to have that amount of money laying around.

An expense like that falling on you can definitely ruin your life.

{kind=link}

I did the math in the USA. When I was married with kids my effective rate for a the highest year was 52%. My last year as a single male and all kids over 26, it was 46%. Effective, not marginal, because that matters in the USA as we don’t track those “other salary deductions” for taxes. Effective for those ready to argue include stupid shit like deductibles, copays, uncovered care, out of network care (that happens more than you think with kids). one year we spent 40k (max. In network deductible) because one of my kids had a spiral fracture of his leg on a growth section that had he not endured 3 (THREE) surgeries, he would be left side shorter. That was 190k for all surgeries and 40k out of pocket. Dental, HSA, FSA, Vision, Medical… People need to realize that even though its pre tax, you’re still paying for it and that needs to be considered for effective rate.

I was offered a job in Denmark, so I know this for fact: Denmark was a near match at marginal rate to USA effective rate assuming I never needed critical care in the USA (i would be in debt). BUT, Denmark has effective tax rates in the 40% for those making less than 85k (USD). I think there’s a rich person tax above that at 49%, but I never accepted the job because my Ex wife was a shithead so I didn’t find out.

I’m now in spain paying around 47% effective, but get Beckhams law will make that be 24% at tax time for the next 10 years. After that I need to pay like everyone else and at 10 years I get a pension (small one) for spain.

So yes, Americans pay more. Waaaaay more.

Correction: We pay waaaay more for waaaay less.

That is a perfect Tl;dr. Heh

190k is a very large amount, I’m not sure if by 40k out of pocket you mean the insurance covered the rest.

Still, 40k is a lot of money and 190k is pretty much my salary for the next 10 years. I’m sure jobs are a bit better paid in the US; but I’m also quite convinced it is not that common to have that amount of money laying around.

An expense like that falling on you can definitely ruin your life.

I borrowed money to pay for it. I was lucky, very lucky.